VW AG (VOW3) and Porsche SE (PAH3): NAV Discounts That You Can Eat

“It has been demonstrated time and time again that no asset is so good that it can’t become a bad investment if bought at too high a price. And there are few assets so bad that they can’t be a good investment when bought cheap enough.” - Howard Marks

"It's not hard to find good news or good prices, but you can't find both in the same package." - John Neff

Important disclaimer: I don’t expect to be able to sell the stock at a higher price anytime soon or at all!

Introduction

It’s only apt to start this write-up with not one but two investor quotes, a disclaimer, and a meme, in an effort to compensate for the fact that this thesis combines two of the greatest value traps of all time: Auto OEMs and family-holding/SOTP/NAV discounts. It’s a value trap within a value trap. A deep value investment, only suitable for true connoisseurs of losing money the intelligent way, how Ben Graham intended it.

Auto OEMs are terrible businesses. They guzzle capital like an old clunker guzzles oil, yet deliver exceptionally low returns on that capital. They pour billions into CapEx to keep production plants running and shovel just as much into R&D only to stay competitive. Earnings are always overstated—CapEx constantly outpaces depreciation, and capitalized R&D expenses exceed amortization. In reality, the only earnings you can count on are the dividends in your pocket; everything else is an illusion. When demand drops, their high fixed costs eat up all the margin, and thanks to strong unions, they can't easily scale down the workforce to match demand.

As if things couldn’t get worse, let’s add a governance structure that’s misaligned with shareholder’s interests. Half the board of directors (10 out of 20 seats) consists of employee representatives who don’t own shares in the company. Of the other half, 2 seats belong to the state, which owns 13% of economic interest and 20% of voting rights, but effectively acts as another employee representative. Meanwhile, the family that owns 32% of economic interest and 53% of the voting rights, gets a total of 3 out of 20 seats.

But don’t worry—you can “align” yourself with the family by owning their holding company! Except, of course, only the non-voting shares are publicly traded, so you’re just along for the ride in whatever they’re doing. And the management you’re counting on to allocate capital effectively at the holding level doesn’t hold any meaningful amount of shares in the holding either.

Naturally, I’m talking about the Volkswagen Universe.

Summary

All that being said, I believe VW AG is undervalued, both on a sum-of-the-parts basis and, more importantly, in terms of the cash I expect to get out of the business in the form of dividends. Since 2006 (as far back as my TIKR data goes), the average dividend yield has been 3%. Today, it’s sitting at 10%—a 70% discount to the historical average. The discount to the SOTP is also around 70%. If things go right, I see up to 200% upside in VW.

But that’s not the end of the story. You can get both VW AG (VOW/VOW3) and Porsche AG (P911—the carmaker) at a 34% discount by going through Porsche Automobil Holding SE (PAH3), the holding company of the Porsche-Piëch family that owns 31.9% of VW’s economic interest (53.3% of voting rights) and 12.5% + 1 share of Porsche AG’s economic interest (25% + 1 of voting rights) with look-through majority control of Porsche AG.

To put it another way, you're essentially getting the VW AG stake, minus the holding debt, at market value—and 80% of the Porsche AG stake for free.

However, I’m perfectly fine if VW shares never appreciate to their sum-of-the-parts value (or even anywhere close) and if the NAV discount at the holding level never closes (life is much easier with low expectations). All I’m asking for is to collect the increasing dividend income that Porsche SE receives from its VW and Porsche AG holdings, i.e. €1.7 billion, or €5.50 per Porsche SE share for 2024 —a 13% yield on the current share price of around €40 (more on Porsche SE capital allocation later).

Alternatively, you can buy VW AG preferred shares (VOW3) at a 10% dividend yield and sacrifice some yield for the benefit of not having to worry about capital allocation at the Porsche SE level.

I like both shares but Porsche SE in particular because the NAV discount is not just theoretical but results in a higher yield and thus more money in your pocket (with a caveat - see capital allocation section).

Investment Thesis

(1) Consistent Dividend Growth

As I mentioned, I only trust the earnings of Auto OEMs to the extent that they go straight into my pocket. Fortunately, VW is a consistent dividend grower, currently maintaining a moderate payout ratio of 28%. The dividend per share has increased by 12% per annum since 2005. While VW has historically traded at a 3% dividend yield, today’s yield is around 10%.

Including the special dividend of €19.06 per share from the Porsche IPO proceeds in 2022, the preferred shares of VW (VOW3) have paid out €44.44 per share between 2021 and 2023. That’s nearly half of the current share price of around €90 for the preferreds.

Currently, VW will invest about 14.5% of its automotive revenue in CapEx and R&D in 2024 (FY24 is expected to be the peak year in terms of expenditures), converting only around 35% of its automotive operating results into cash. They aim to reduce the investment rate to 11% and increase cash conversion to 60% over the medium term, all while boosting operating margins. Their goal for the dividend payout ratio is to exceed 30%. Ideally, this means the dividend continues to grow through a combination of improved margins, greater capital efficiency, and a slightly higher payout ratio.

Porsche AG does not yet have a long history of paying a growing dividend as a public company. However, Porsche AG intends to distribute an annual dividend in the medium term of around 50% of the group result after tax.

Historically, Porsche SE has distributed nearly all of its dividend income to shareholders. More recently, however, they’ve opted to maintain a dividend of €2.56 per share, which is less than half of the dividend income of €5.50 per share, prioritizing debt repayment with the excess cash. The family took on significant debt of €10.1 billion (having no substantial debt prior) to acquire the direct stake in Porsche AG from VW in 2022. They immediately paid down a large chunk with the special dividend of €19.06 per share that VW distributed to its shareholders from the proceeds of the Porsche AG IPO, leaving Porsche SE with around €7 billion of net debt immediately following the transaction.

As of June 30, 2024, Porsche SE has already reduced its net debt to €5 billion, thanks to regular dividends from both VW and Porsche AG. (More on Porsche SE capital allocation later.)

(2) A Valuable Portfolio of Brands

The individual brands are segmented into different brand groups. First, there’s the Core Group, which includes the VW brand, VW Commercial Vehicles, Škoda, and Cupra/SEAT. These are the volume brands. They typically have the lowest margins, the least pricing power, and face the most competition. Cupra, however, stands out as a hot new brand incubated within SEAT, making waves in Europe with impressive growth.

Next is the Progressive Group, which consists of Audi, Lamborghini, Bentley, and Ducati. Needless to say, Lamborghini is an extraordinary luxury asset and one of the crown jewels of VW’s portfolio. With just 10,112 vehicles sold last year, generating €2.7 billion in revenue, the average selling price of €260k is almost in Ferrari territory—Ferrari’s ASP is around €300k, and it trades at over 40x EBIT in the stock market today. Bentley comes just below that with €2.9 billion in revenue and 13,560 deliveries in 2023, with an ASP of €220k. Both Lamborghini and Bentley have been incredible success stories over the past few years, achieving operating margins north of 20%. Audi, on the other hand, is currently struggling, but it still holds its place alongside BMW and Mercedes-Benz as a german premium car brand.

Porsche, which I like to think of as the Rolex of cars, is another crown jewel in VW’s portfolio. It sits in its own category—the Sport Luxury Group. While it’s facing some headwinds after a run of record results in the Covid/post-Covid years, Porsche’s ASP of around €100k puts it in a unique position. It’s priced between the premium brands like BMW, Mercedes, and Audi (with ASPs around €50k) and the high-end luxury brands like Bentley, Lamborghini, and Ferrari. I have no doubt that Porsche will maintain its prominent place in the luxury automotive landscape for decades to come despite the temporary slow-down.

Then there's the Truck Group—Traton, which includes Scania, MAN, VW Truck & Bus, and Navistar. The Traton Group was spun off and listed separately on the stock exchange in 2019, though VW still holds just under 90% ownership. Scania stands out as a key asset, often likened to the Harley-Davidson of trucks. It consistently boasts operating margins north of 12%, which is significantly higher than its German sibling, MAN, and well above Traton's overall margin of 8%.

And lastly, we have VW Financial Services, the group's internal financing arm. It’s always been a reliable moneymaker, with a historical return on equity in the high single to low double digits range.

My conservative estimate of the total equity value of this whole portfolio is around €160 billion. VW’s total market cap currently sits at around €47 billion.

You can get another 34% discount through Porsche SE.

(3) Determined Management

The management team, led by CEO Oliver Blume and CFO Arno Antlitz, is taking bold steps—unprecedented in recent VW history—to cut costs and secure the group’s profitability and competitiveness. Recently, management terminated a long-standing employment security agreement, originally set to last until 2029, which had been in place since 1994 and prohibited operational layoffs. They’re planning to close two plants in Germany to adjust the fixed cost structure to Europe’s structurally smaller auto market.

However, the powerful employee representatives have made it clear they won’t agree to any plant closures or layoffs. With tariff negotiations between the two parties set to begin at the end of September, both sides have established their positions.

You might think plant closures and layoffs are regular measures in a tough economic climate, but for VW, this is unprecedented. And it’s a risky move given VW’s board structure—12 of the 20 board seats belong to employee representatives and the state of Lower Saxony. A two-thirds majority is enough to change the CEO, so management is walking a fine line between managing profitability and long-term competitiveness, and keeping the workforce and powerful employee representatives content by avoiding job cuts.

From a shareholder’s perspective, I see these unprecedented measures as a positive sign. It shows that management is determined to make tough decisions for the sake of long-term value.

Risks

(1) China

Let’s break this down into two parts: (a) the profit pool in China and (b) the profit pool in Europe.

(a) China’s Profit Pool

VW was one of the first foreign auto OEMs to enter China 40 years ago. Today, VW holds a 20% market share in ICEs, but ICEs are quickly losing relevance, particularly in the Tier 1 and 2 cities, in favor of BEVs and PHEVs. In the BEV market, VW isn’t currently a major player in China, and its overall market share has declined to 14%. This decline has been reflected in the company’s financial results for some time now.

At its peak in 2015, VW’s Chinese joint ventures contributed over €4 billion to profits—nearly half of the normalized operating results of the rest of the group at the time. However, this figure has steadily declined. In 2023, profit contribution from Chinese JVs dropped to around €2 billion, accounting for just 10% of the operating results of the rest of the group. Meanwhile, VW’s overall operating results more than doubled during the same period, more than compensating for the drop in Chinese JV profits.

However, this doesn’t tell the full story, as it understates China’s significance to the group. The JVs primarily produce Core Group and Audi vehicles locally, but Porsche, Bentley, Lamborghini, and some high-end Audis are exported to China, with those results fully consolidated into VW’s operating profit. China is and will remain a very important market for VW.

To that end, VW has started developing and producing cars independently in China, outside of its traditional JV partnerships. The new, fully-owned Chinese subsidiary, VCTC (that’s also launching car models in partnership with local OEM Xpeng soon) aims to develop and manufacture vehicles tailored for the Chinese market, competing head-on with local players. VW plans on regaining market share in the coming years.

(b) Europe’s Profit Pool

Now, let's talk about Chinese automakers encroaching on VW’s home turf in Europe. Brands like BYD have made waves with affordable, high-quality BEVs and PHEVs, like the Seagull that’s available in China for under €10k and is supposed to be offered for under €20k in Europe. However, I don’t believe that Chinese competition should be a material threat to VW in Europe. It is a threat of course and VW has to improve and compete with these new players, but we’ve seen this before—the Japanese OEMs massively expanded globally around the 1980s, and the Koreans followed in the 2000s. The new wave of foreign competitors initially competing on price is not unprecedented in the auto industry. VW weathered all of those storms before.

VW is launching its own lineup of EVs priced below €25k in Europe by 2026, which should help it compete in the more affordable segment of the market.

While Chinese OEMs are now facing tariffs from the EU, they’ve already started opening manufacturing plants in Europe, with locations in Eastern Europe and Turkey. But producing cars in Europe comes with its own unique challenges—not just in terms of cost, but also in navigating complex regulations and labor markets. We will see how this pans out for the Chinese OEMs.

All things considered, China is definitely one of VW’s biggest challenges right now, but it’s not an insurmountable one.

(2) EV Transition

The main problem with EVs is that they’re still too expensive, the charging infrastructure remains inadequate in certain regions, and the resale value of current-generation EVs is low due to concerns over battery durability and the anticipated improvements in future battery technology. Legacy ICE OEMs, like VW, face an additional challenge: they’re barely making any money on EVs. Increasing BEV sales is currently dilutive to margins, but it’s a necessary move to comply with regulatory requirements and avoid penalties.

According to management, ICE and BEV margins will approach parity, driven by lower R&D expenses from platform synergies, battery cost savings, and economies of scale along with more efficient manufacturing. At VW's Capital Markets Day in 2023, management indicated that much of the margin gap would close with the introduction of the SSP platform in 2026. However, I suspect this will take longer than anticipated. ICE vehicles are likely to remain the high-margin cash cow for some time, while BEVs continue to weigh on overall profitability.

There’s a lot of uncertainty surrounding the EV transition. VW’s management has signaled a more balanced approach going forward, serving a broad range of customers instead of focusing all of their efforts on a single technology. EVs are the future and that’s the way VW will go, but many customers in different markets will continue to drive ICEs for a long time. We’ll have to see how policy and regulation shape the market. Much of it is unknowable. That said, I’m confident that with VW’s sheer financial firepower (investing over €30 billion in CapEx and R&D annually) and the strength of its brands, the company can adapt to whatever lies ahead.

(3) Capital Allocation at Porsche SE

Porsche SE is set to earn €1.7 billion (or €5.50 per share) in dividends this year. Of that, they’ll pay out €783 million (or €2.56 per share) to shareholders, which translates to about a 6.4% yield. The majority of the remaining cash will be used to continue paying down debt. It’s unclear what the target debt level is, but before acquiring the direct stake in Porsche AG, Porsche SE had no meaningful debt. For now, I expect they will keep the dividend steady for a while until the debt is reduced further.

Additionally, Porsche SE is making efforts to diversify its portfolio beyond its core holdings in VW and Porsche AG. They’ve been making smaller investments—typically up to a low triple-digit million range annually—into startups in the mobility and industrial technology sectors. What reassures me is that these investments are small, within their circle of competence, and they are co-investing with highly regarded firms like EQT and KKR.

While I would personally prefer that Porsche SE distribute all of its earnings as dividends, management has expressed a desire to diversify and transform into a broader investment platform in the long term. As long as they maintain a focus on paying out most of their earnings as dividends, raise the dividend once debt reaches a target level, and keep investments small and within industries they understand, I’m comfortable with this approach.

Recent investments include a low double-digit million euro investment in Flix, alongside EQT, which is a market leader in long-distance bus travel across Europe, North America, and Turkey. They also recently invested in Waabi, a Canadian company working on AI-driven solutions for self-driving trucks. These investments are relatively small and focus on Porsche SE’s expertise in the mobility space.

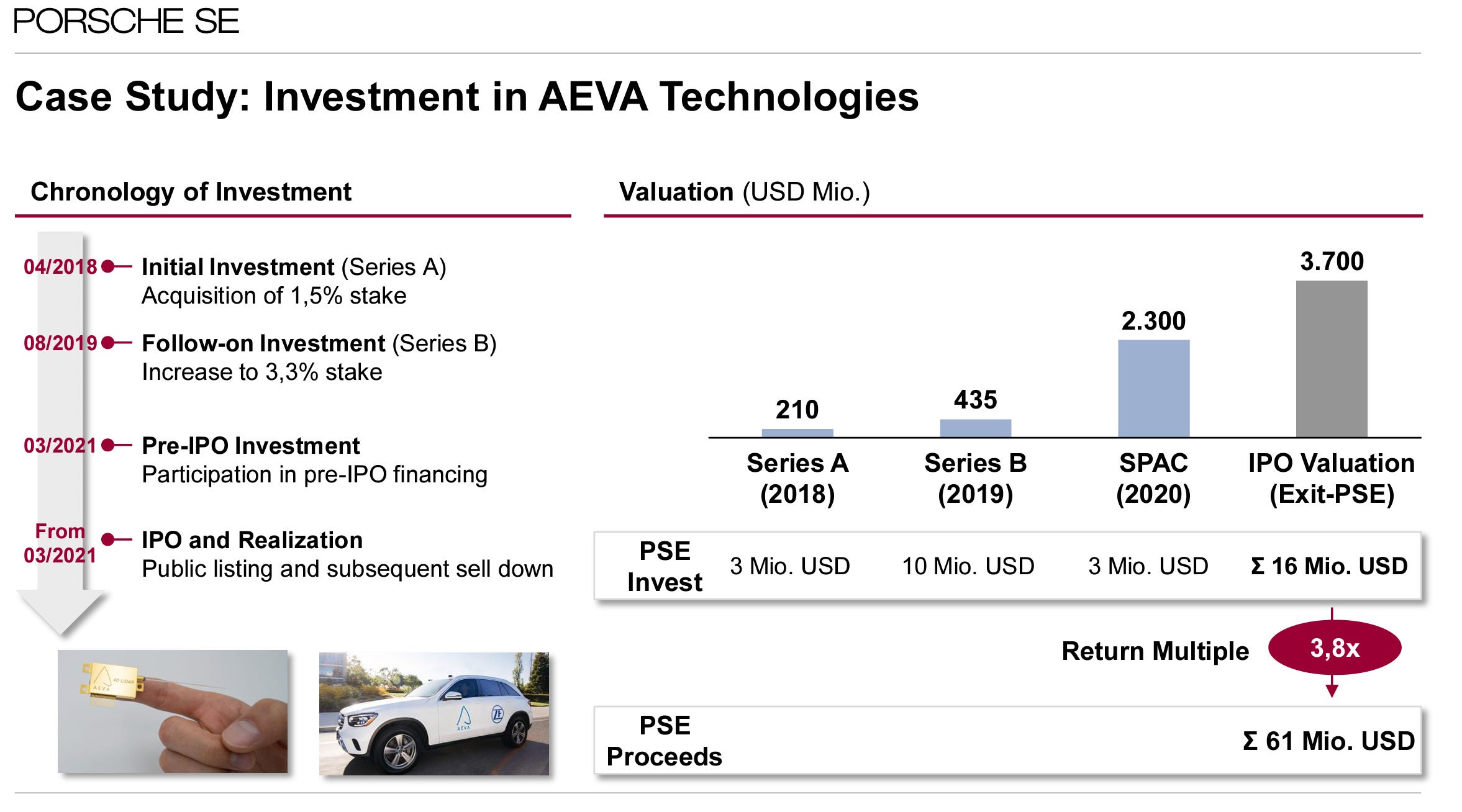

One example of a successful investment from entry to exit is AEVA Technologies, where they made nearly four times their money within three years.

However, I should note that AEVA stock is down over 90% since the IPO and PSE’s exit.

Conclusion

I firmly believe VW represents one of the biggest dislocations between price and value in today’s market. While unlocking that value isn’t easy, it at least provides a real margin of safety and a floor to the share price. Yes, there are risks—the governance structure is convoluted, Chinese competition is fierce, and the EV transition adds uncertainty. Yet, despite these challenges, the stock is priced where the risk is more than compensated. With a 10% dividend yield, a portfolio of premium and luxury brands, and management showing unprecedented intent to tackle inefficiencies, VW AG offers an attractive opportunity for patient investors. Through Porsche SE, the opportunity becomes even more compelling, with a higher yield and a significant discount to the underlying value of its holdings.

Ultimately, I’m not banking on a short-term rerating or expecting the NAV discount to close overnight. I’m here for the dividends—solid, growing cash flows straight to my pocket.

Great write up,

I’m invested in Porsche Se myself since I love the multiple layers of potential revenue creation, especially the leverage on the holding level.

Two things I would add:

1. You should definitely take a closer look on the History of Porsche and Volkswagen as company’s combined. First of its super interesting with the fight for Power, both companies trying to take over each other and a squeeze out with for a super short Periode of time even made Volkswagen the most valuable company of the World.

In the end you have the Family Porsche / Piëch controlling Porsche through Volkswagen as a result of the failed takeover of Volkswagen. They see themselves as the inherit of Freddy Porsche and their ultimate goal is to take back control of Porsche (independently). The first step of this was the IPO of Porsche in 2022 to establish a stand alone presence on the stock market. I see a good chance that in the future there is some kind of deal that trades most or some of there Volkswagen shares for a more Porsche shares or even a total separation of the two companies. They care way more about Porsche than Volkswagen. Also a break up of the complex structure would create Value for all Parties.

2. I think you shouldn’t underestimate the political component in this case. Lower Saxony is highly dependent on Volkswagen, a lot of jobs at Volkswagen and the surrounding Company’s depend on Volkswagen. After Elections one of the exit pole questions even is: „Which Party trust the most to lead Volkswagen successfully ?”. The political implications of closing a plant in Germany itself, which never happened before are huge. Politically this steps would only be possible if there’s some kind of dividend cut, at leaset for some time.

Great write up. thanks!