Petershill Partners PLC (PHLL.L): GP Stakes at a Discount

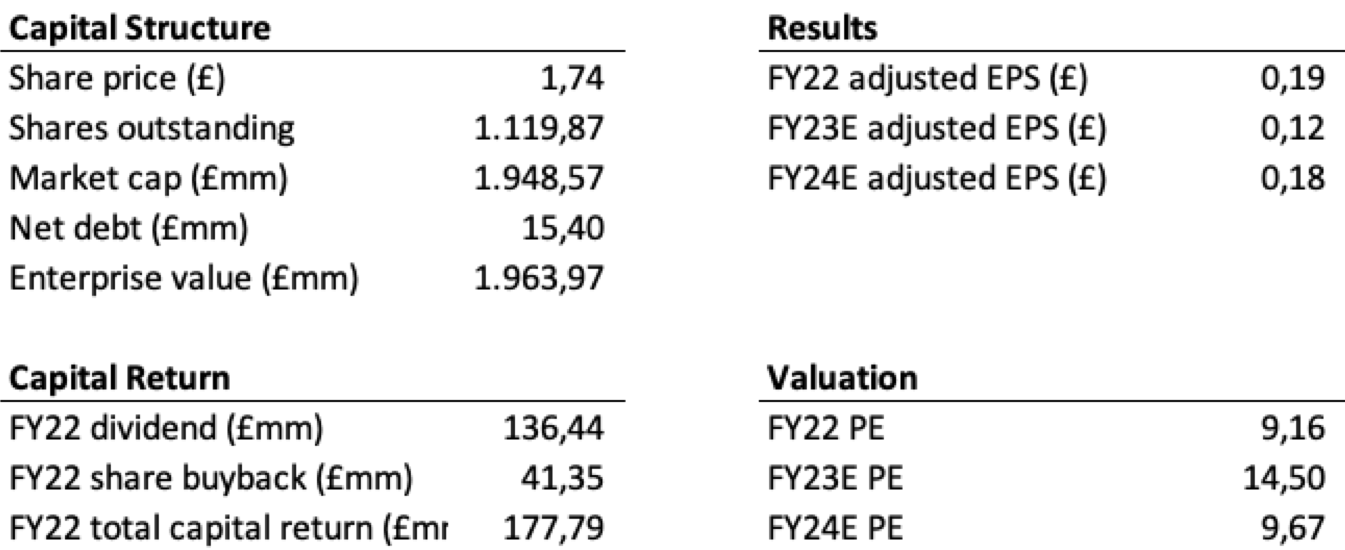

Financial Snapshot

Investment Thesis

Private capital firms are exceptional businesses. They earn significant fees from long-term, locked-up capital, providing steady, recurring earnings with minimal initial investment. Imagine teaming up with top-performing General Partners (GPs) in the industry and sharing in their profits; this is the opportunity Petershill Partners PLC presents.

Petershill Partners holds minority stakes in 25 mid-sized private capital firms managing over 200 funds across various strategies and asset classes. By investing in these high-quality, high-performing alternative asset managers, the company secures stable, recurring earnings. Notably, the assets under management (AUM) of partner firms have grown at an impressive 28% compound annual growth rate (CAGR), from US$104 billion in 2018 to US$283 billion in 2022, surpassing industry growth rates by 10 percentage points. Partner firms consistently outperform benchmarks on a net Internal Rate of Return (IRR) basis, especially in private equity, which represents the largest segment by AUM.

Recognizing the talent-driven nature of these firms, Petershill Partners maintains non-controlling partnerships to preserve the entrepreneurial spirit of its partner. Management of these firms retain majority ownership to ensure alignment and motivation for performance and business growth. To mitigate the drawbacks of non-controlling interests, Petershill structures minority stakes with contractual protections that have significant advantages over common equity, ensuring participation alongside, not after, management.

The business is simple and highly cash-generative. Revenue streams from partner firms consist of management fee income (~70-80%), performance fee income (~20-30%), and realized investment and balance sheet income (~0-10%). Management fees primarily come from long-term private capital commitment funds with high visibility and recurrence. Due to the high level of diversification across strategies and vintages, performance fee income is earned regularly from a wide range of funds, making them quasi-recurring.

The company has no employees of its own and is managed entirely by the Petershill Group within Goldman Sachs, leveraging a strategic partnership for proprietary sourcing, an invaluable network, and value creation through a dedicated GP Services team. In turn, Goldman Sachs receives recurring operating charges quarterly, amounting to 7.5% of the Group’s investment income. This results in a thin layer of expenses, enabling 85-90% EBIT margins and strong free cash flow conversion. However, the close relationship with Goldman Sachs poses significant governance risks, which will be further discussed in the risk section.

Petershill Partners' organic earnings growth aligns with partner firms' AUM and fee income growth. Partner firm management fees have grown by 28% annually since 2018 in line with fee-paying AUM. Private market AUM is forecasted to maintain a 10% CAGR until 2027, driving Petershill Partners' organic earnings growth. The company aims to invest US$100-300 million annually in new stakes, targeting low teens entry multiples of distributable earnings. Since the IPO in September 2021, the company has invested US$638 million across eight acquisitions. However, due to the substantial decline in its stock price by 50% since the IPO, the company has prioritized buying back shares, reducing shares outstanding by around 3%, and adding no further stakes in 2023.

At the current share price, Petershill Partners offers an attractive entry point to a diversified portfolio of quality mid-sized private capital firms typically inaccessible to public market investors. Investors can reasonably expect a combined 20% annual return from dividends, buybacks, and organic growth over the medium term, before factoring in accretive future acquisitions and a potential valuation rerating.

It’s in Goldman Sachs's reputational and financial interest, through performance fees for the underlying funds and the operating charge earned on the company’s investment income, to ensure the success of Petershill Partners PLC and set a successful precedent for future public listings of its GP stakes.

Company History and Industry Overview

Since its inception in 2007, the Petershill division within Goldman Sachs Asset Management has become a leading investor in GP solutions, specializing in providing growth capital to alternative asset managers through acquiring minority ownership stakes. These investments aim to support long-term value creation by offering strategic capital for various purposes, including employee retention, business development, and buying out legacy equity holders.

The GP solutions industry has experienced rapid growth post the global financial crisis. Partnering with a GP solutions investor offers several benefits for GPs. Larger alternative asset management firms and bigger funds often require increased GP commitments, and new products/strategies may demand additional capital. GP solutions investors offer permanent capital and strategic support to partner firms while allowing original owners to retain control, maintaining alignment between management and ownership. Additionally, equity capital injections accelerate growth without the constraints of debt- or self-financing or the reporting requirements of public listings/IPOs.

The growth of the GP solutions industry has been led by established players such as the Petershill Group within Goldman Sachs, Blue Owl/Dyal Capital, and Blackstone Strategic Capital Holdings.

Entry into the GP solutions industry presents high barriers, with General Partners being highly selective in their choice of partners. GP solutions investors must demonstrate the necessary scale, stability, and resources to provide value-added services. Moreover, traditional providers of external private capital may be considered competitors, limiting partnership options (think Sixth Street’s bid to block the Dyal-Owl Rock merger).

The following slide from Blue Owl’s investor day presentation outlines the competitive landscape of the GP solutions industry. Goldman focuses on the attractively valued and fast-growing mid-market segment.

It's important to note that Petershill Partners PLC is not a spin-off of Goldman Sachs's GP solutions business but represents the public listing of select assets from Petershill II, III, and Goldman Sachs's Vintage VII private funds, and related entities (collectively, "Petershill Funds"). This listing offers partial realization of investments, liquidity, and access to capital markets for Petershill Funds investors, who indirectly hold over 75% of Petershill Partners PLC's issued shares.

Moreover, the public listing of Petershill Funds assets provides strategic advantages, including a permanent capital source for partner firms, institutionalizing Petershill Partners Group's investments, facilitating M&A opportunities, and enhancing flexibility for follow-on investments and GP commitments.

Goldman Sachs aims to align Petershill Partners PLC with its private funds, intending for Petershill Partners to co-invest alongside them. The most recent GP stakes fund, Petershill IV, closed at $5 billion in January 2022 and has co-invested with Petershill Partners PLC. The IPO prospectus states that the company will co-invest alongside all future private funds raised by Goldman Sachs with the same strategic focus. See also the Joint Acquisition Framework outlined during an investor webinar below.

Risks

Investing in Petershill Partners PLC comes with its own set of risks, primarily associated with its close ties to Goldman Sachs, the company that runs the show. Here are some things to watch out for:

Dependence on Goldman Sachs GP Services Franchise: Petershill's success, from sourcing new deals to providing value-add services to partner firms, relies heavily on its partnership with Goldman Sachs. If this relationship ends, Petershill will lose its competitive edge as a GP investor, impacting its future prospects, and may even require it to exit certain existing investments.

Risk of Changing Terms: The deal between Petershill and Goldman Sachs is favorable for Petershill right now. The operator agreement has an initial term of seven years (ending 2026), after which it will automatically renew on an annual basis until terminated by either party. If the terms change, especially the 7.5% operator charge, which essentially constitutes the entire OpEx of the company, it could eat into Petershill's profits.

Management Focus: Goldman Sachs GP solutions team has a lot on its plate, including managing new private funds like Petershill IV. This could mean less attention on Petershill Partners, which might affect its performance.

Ownership Overhang: Right now, Goldman Sachs owns over 75% of Petershill Partners through its private funds on behalf of LPs. But Goldman is required to realize the remaining investment for its LPs within five years of Petershill’s listing (i.e. September 2026). How they'll do this exactly isn't clear yet.

Goldman Sachs's incentives play a crucial role in mitigating these risks. Here's why:

Financial Incentive: Goldman stands to benefit financially from Petershill's success, as it earns performance fees from the Petershill Funds. Therefore, Goldman has a vested interest in seeing Petershill's stock price rise.

Reputational Incentive: Ultimately Goldman Sachs wants to keep its investors happy and set a good example for future deals. Presumably, a lot of the same LPs from the Petershill Funds, are expected to invest in future private GP stakes funds. From a reputation perspective, it’s in Goldman’s best interest to make sure things go smoothly with Petershill Partners.

Co-Investment Synergies: Leveraging Petershill as a co-investment vehicle for its private funds gives Goldman more capital and firepower without taking up any additional resources.

Setting Precedence: Petershill Partners' success can serve as a model for future private GP stake funds realizations.

Then there’s the risk of entering a prolonged downturn in private capital fundraising and realizations. This could lead to subdued growth in management fees and failure to realize performance fees.

However, several factors help mitigate this risk:

Diversification: Petershill Partners has a broad diversification across different firms, funds, and strategies. With investments in 25 firms and over 200 underlying funds spanning private equity, private credit, real estate/assets, venture capital, and absolute return, the likelihood of some performing well at any given time is high.

Recurring FRE: The steady income generated from management fees on locked-up capital alone provides a reliable revenue stream, ensuring sizeable earnings even during periods of weak realizations. Management fee income alone should reach around US$270 million for FY24. This estimation is calculated by multiplying the FY24E FPAUM of US$229 billion by the blended partner firm ownership of 13.5%, the partner blended net management fee rate of 1.41%, and the average partner FRE margin of 62%. After accounting for the operator charge to GS, other operating expenses, and interest expenses, pre-tax earnings per share should be around GBP 0.14 from management fees alone. Considering this, Petershill Partners trades at under 13x pre-tax earnings from a growing stream of management fees.

Variable Cost Structure: The operator charge to GS is not fixed but rather tied to Petershill’s investment income. This means that during challenging times, operating expenses are reduced proportionally with a decrease in income.

Long-Term Industry Growth Supported by High Returns: Despite short-term fluctuations, the long-term performance of alternative asset managers and funds remains strong. This performance supports the ongoing trend of increased allocation towards private capital, as indicated by industry reports, as well as continued strong management fee rates.

Conclusion

Despite potential risks such as the dependence on Goldman Sachs and the possibility of prolonged market downturns, Petershill Partners is well-positioned to navigate challenges and capitalize on opportunities in the evolving private capital landscape. With strong financial incentives for success and a commitment to setting precedents in the industry, Petershill Partners PLC represents an attractive investment for those seeking exposure to the private capital sector.

In summary, Petershill Partners offers investors the opportunity to participate in the success of top-performing alternative asset managers, providing a pathway to attractive returns through dividends, buybacks, and organic and inorganic growth.

Note to US investors: Petershill Partners PLC is a Passive Foreign Investment Company (PFIC) for US-taxable investors.

Disclaimer: The author of this publication is not a licensed investment professional. Nothing in this newsletter is investment advice. Do your own due diligence.